Financial Accounts second quarter 2024

Households continued to save while the growth rate of mortgage loans increased

Statistical news from Statistics Sweden 2024-09-19 8.00

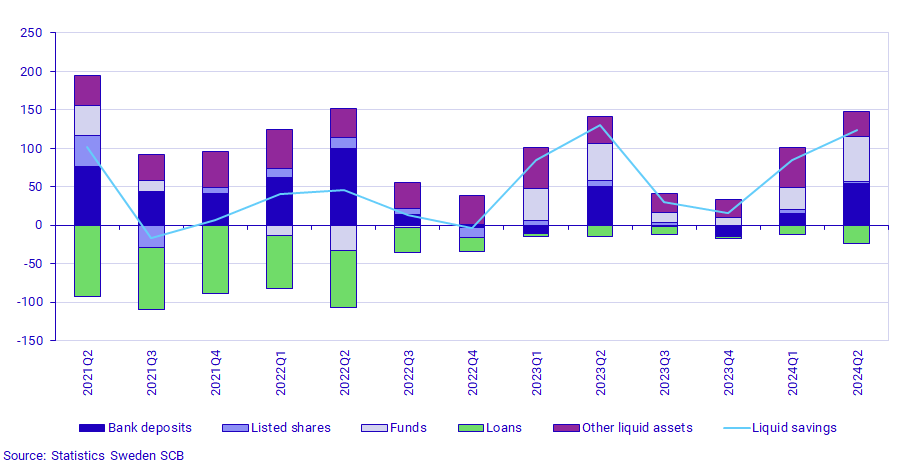

Household liquid savings amounted to SEK 123 billion in the second quarter of 2024, which is a similar level as in the second quarter last year. The annual growth rate of households' mortgage loans increased for the first time since 2021.

There is a seasonal variation in household savings, where savings are usually highest in the second quarter. This is due to the payment of tax refunds, but also that share dividends are high during this quarter. Household liquid savings in the second quarter of 2024 amounted to SEK 123 billion, which is a similar level as in the second quarter last year.

Household savings in funds and net deposits in bank accounts were high, amounting to SEK 59 billion and SEK 55 billion respectively. Large net purchases of funds made by households in the second quarter can partly be explained by the fact that retained earnings are reported as purchases of new fund units. Retained earnings are dividends and interest income that the funds receive and then reinvest for the unit holders.

Growth rate of households' mortgage loans increased

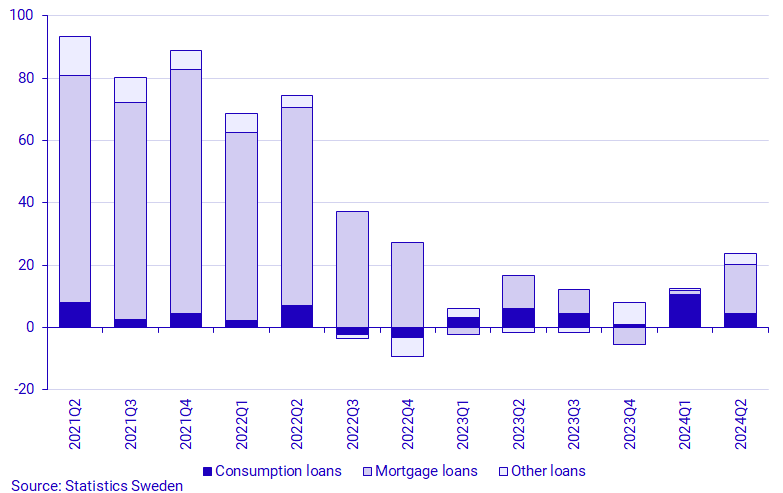

Households borrow primarily to buy a residence, but loans also finance part of their consumption. Statistics on the purpose of the loans are not collected by Statistics Sweden, but the breakdown based on the collateral of the loans can be used to approximate the purpose.

Households' total net borrowing, i.e. their new loans minus amortization, was relatively high in the second quarter and amounted to SEK 24 billion. This is an increase of SEK 11 billion compared to the previous quarter and an increase of SEK 9 billion compared to the corresponding quarter in 2023.

During the second quarter, households' net borrowing amounted to 16 billion in mortgage loans, 5 billion in consumer loans, and 3 billion in other loans. The increase in mortgage loans is the highest observed in a quarter since the fourth quarter of 2022.

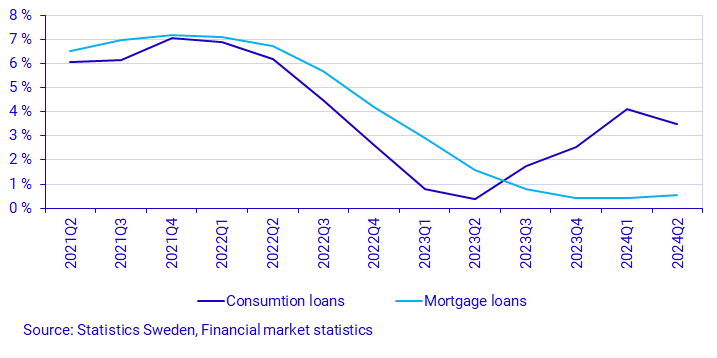

In the second quarter, the annual growth rate of households' mortgage loans from monetary financial institutions (MFIs) was 0.5 percent, representing an increase of 0.1 percentage points compared with the previous quarter. This is the first time the growth rate has increased in a quarter since the fourth quarter of 2021.

Consumer loans grew at an annual rate of 3.5 percent. Consumer loans account for only 6 per cent of households' total loans from monetary financial institutions (MFIs). Consumer loans are, however, the type of loan that has increased the most in previous quarters.

Financing of non-financial corporations

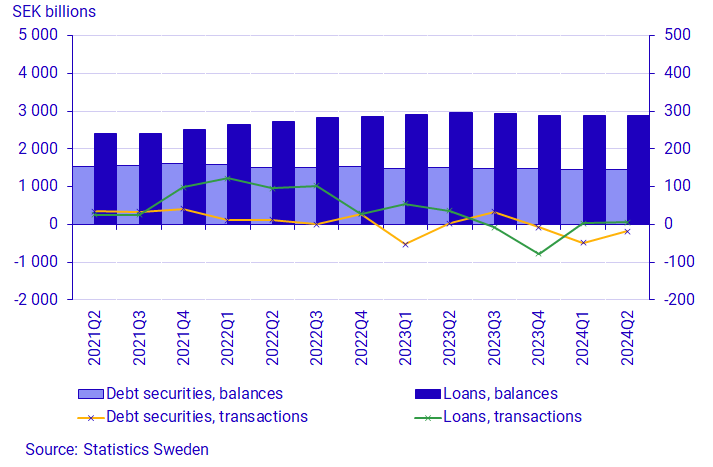

During the second quarter of 2024, the value of non-financial corporations' financing through loans, i.e., new loans minus amortization from monetary financial institutions, was 6 billion SEK. This is an increase of 3 billion compared to the previous quarter, but a significant decrease from the corresponding quarter of the previous year, when this value was SEK 36 billion.

Financing through interest-bearing securities, i.e. through new issues minus maturities and repurchases, amounted to SEK -18 billion. This is SEK 31 billion higher than in the previous quarter and SEK 21 billion lower than in the corresponding quarter last year.

Total loans from MFIs amounted to SEK 2 883 billion at the end of the quarter. The value of issued debt securities amounted to SEK 1 448 billion.

Revisions

In the publication of the Financial Accounts for the second quarter of 2024, revisions have been made back to 2020 in order to improve the statistics where new data have become available. The revisions affect both the time series for years and quarters.

Structural business statistics (FEK) has been revised back to 2022. Economic statistics use, from reference year 2022, the new interpretation of statistical units.

For the local government, the entire time series has been revised for long-term loans on the liability side. The revision is due to municipalities reclassifying old operating lease agreements as financial lease agreements. The full year 2023 has been revised with an annual source.

The central government has been revised with new data from the Swedish Financial Management Authority (ESV), including general pension contributions, from 2005, and emission allowances from 2012.

The foreign sector has been revised back to 2020 with new data from the Balance of Payments.

Definitions and explanations

In the statistical news, reference is made to the liquid financial savings of households. It is calculated as the difference between transactions in financial assets and liabilities excluding accruals (tax accruals, occupational pensions and other technical provisions). For more information, see the Financial Accounts Quality Declaration, section 1.2.2.

The aim of financial accounts is to provide information on financial assets and liabilities as well as changes in financial savings and financial wealth for different sectors of society. The statistics are presented in current prices and do not take inflation into account.

The financial savings in financial accounts is calculated as the difference between transactions in financial assets and liabilities. In the Real Sector Accounts, which, like the Financial Accounts, are part of the National Accounts, financial savings are calculated as the difference between income and expenses. However, financial accounts and real sector accounts are based on different sources, which gives rise to differences between these two products.

In the Financial Accounts, the government debt is calculated differently from the government debt metric that is most frequently reported and which is calculated according to the convergence criteria – the ‘Maastricht debt’. The definition of the Maastricht debt does not include all financial instruments, the instruments are presented in nominal value and the liabilities for government administration are consolidated. The government debt in the Financial Accounts is unconsolidated and includes all financial instruments at market value.

In addition to the government agencies, the government administration sector also includes certain state foundations and state-owned companies. Government administration does not include entities within the retirement pension system. Instead, they make up the social security funds sector. Municipal administration includes primary municipal authorities, regional authorities (formerly county council authorities), municipal associations and certain municipal foundations and certain municipally or regionally owned companies.

More information: National wealth

The National Wealth, which contains annual data on non-financial and financial assets, is also published in connection with the publication of the Financial Accounts. Financial assets and liabilities are collected from the Financial Accounts and are thus consistent with the values published in the Financial Accounts.

For further information, see:

Nationalförmögenheten och nationella balansräkningar (in Swedish) (pdf)

Next publishing will be

The next statistical news will be published on 2024-12-19 at 08.00

Feel free to use the facts from this statistical news but remember to state Source: Statistics Sweden.